What this Means: HB 1300

May 29th, 2026

Another bill that emerged from Committees of Conference this week is HB 1300, another attempt at implementing school district tax caps.

What it does

HB 1300 would require every town and ward in a city to include a tax cap question on its general election ballot in November 2026 and 2028. The question requires a 3/5 majority to pass.

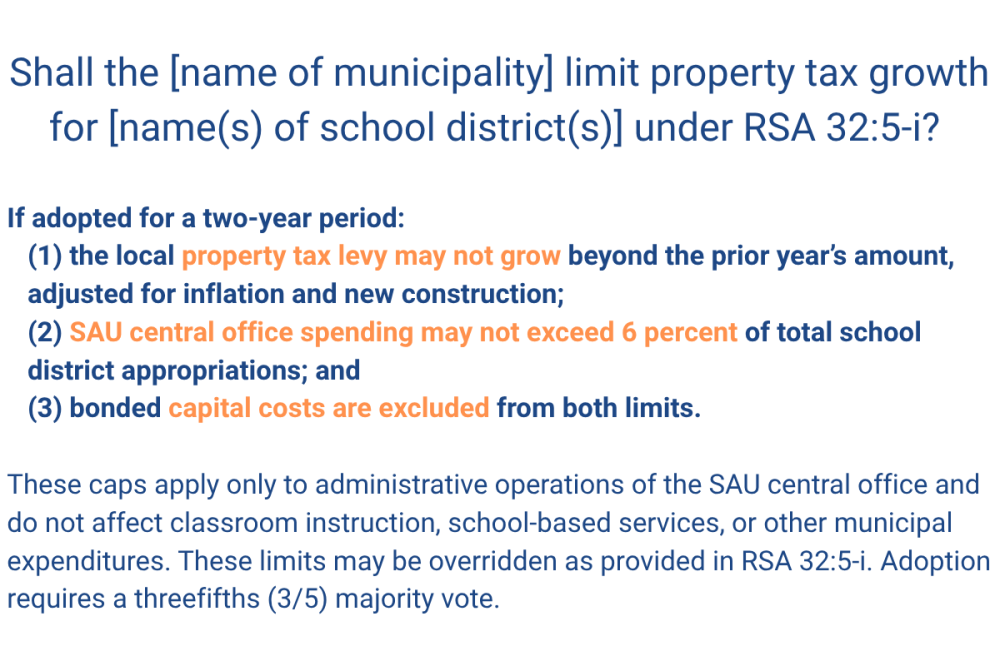

That question must say: “Shall the [name of municipality] limit property tax growth for [name(s) of school district(s)] under RSA 32:5-i? If adopted for a two-year period: (1) the local property tax levy may not grow beyond the prior year’s amount, adjusted for inflation and new construction; (2) SAU central office spending may not exceed 6 percent of total school district appropriations; and (3) bonded capital costs are excluded from both limits. These caps apply only to administrative operations of the SAU central office and do not affect classroom instruction, school-based services, or other municipal expenditures. These limits may be overridden as provided in RSA 32:5-i. Adoption requires a three fifths (3/5) majority vote.”

This means: if 3/5 of the voters who turn out in towns served by a school district vote in favor, school district taxes in that district cannot rise more than the cost of inflation. (There is an allowance for net new taxable property growth, but the Department of Revenue Administration has stated that this number is going to be essentially impossible for many municipalities to calculate in a meaningful way.) If the 3/5 of voters in towns served by a School Administrative unit (SAU) vote in favor, the budget for that SAU cannot exceed 6% of the total appropriations for all school districts in that SAU, with the exception of bonded capital projects. Both of these caps could be overridden by a 3/5 vote at the relevant school district meeting.

Level setting

If you’re confused already, you’re not alone. Before we go deeper, it’s important to call out a few things.

First:

District voters already have the ability to implement a tax cap, should they choose to do so, under RSA 32:5-c. This vote takes place through the usual school district budget process. A small number of districts have adopted such caps, and any district could still choose to do so though the warrant article process.

Second:

The language in the question is confusing. It says “These caps apply only to administrative operations of the SAU central office and do not affect classroom instruction, school-based services, or other municipal expenditures.” And during the Committee of Conference meeting, proponents made the case that the SAU spending cap is important to ensure districts aren’t cutting academics or athletics. But the tax cap and SAU spending cap are two separate things, and there is no guarantee that districts will be able to maintain the same level of services under a tax cap. A district might vote to cap taxes, but the SAU that district is in might not have the votes for the administrative spending cap. That district will still have to pay its share to the SAU, and fund its normal operations with a limited budget. There may also be cases where SAU budgets are already below 6%, which means districts under a tax cap would find other ways to save money. It could be the case that classroom instruction is unaffected, but there is no guarantee.

Third:

The bill defines SAU administration costs as: “expenditures for the general management and administration of a school administrative unit. These expenditures include superintendent services assistant or deputy superintendent services; business administration; human resources; finance; payroll; purchasing; district-level information technology administration; legal services; public relations; and other non-school-based administrative functions, regardless of physical location or building assignment. The term also includes district-level curriculum directors, directors of instruction, or similarly titled positions who are not employed under a collective bargaining agreement or who do not provide direct classroom instruction for more than 50 percent of their work time, as well as any personnel reported to the department of education as employed by the central office.” If that list sounds different from what you’d think of as an SAU budget, you’re not alone.

Fourth:

And finally, it is unclear how long the tax cap lasts. If passed in 2026, the cap is applicable beginning in fiscal year 2028. The question in the legislation says “if adopted for a two-year period,” but nowhere else in the bill does it specify that the cap only lasts two years. We do know that regardless of when the cap is adopted, it would cease to apply in 2032. (Timing is one of the things the two chambers originally did not agree on: the House wanted a vote every two years, but the Senate did not.)

None of these are minor issues, and if this bill passes, someone, likely a school district official, is going to have to figure them out. The added legal costs simply to ensure compliance with an unclear ballot question could end up being the very reason districts need to increase their budgets.

Digging in deeper

With those points of confusion in mind, let’s look at how this process could play out, what the bill really does, and why it might ultimately end up increasing school district budgets.

Timing

The timing is purposefully separate from the usual school district meeting process. Public school skeptics claim that because turnout to school district meetings is lower than general election turnout, decisions are being made that don’t represent the true will of people in a town. But New Hampshire’s school district and town meeting process is a point of pride for many Granite Staters, one of the purest forms of local democracy. Citizens don’t just vote at the school district meeting, they have a chance to interact with decisionmakers, to ask questions, and to propose their own changes. Separating the tax cap decision from the budget process undermines one of our most local forms of governance and makes it hard for districts to plan. (Many districts will have already started budgeting for FY 2028 before finding out if they’re subject to a tax cap based on the November 2026 vote.)

District and SAU boundaries

In a town that has its own K-12 school district, the tax cap is simple: if 3/5 of voters who turn out in the town are in favor, the tax cap is enacted. Likewise, if that district has its own SAU, all it takes is 3/5 of the town’s present voters to enact the 6% SAU appropriations cap.

But in many places throughout the state, it is not quite so simple. Consider SAU 39. This SAU serves 2 towns (Amherst and Mont Vernon) and 3 school districts (Amherst, Mont Vernon, Souhegan). The local education tax in Mont Vernon covers funding for the Mont Vernon school district, but also for Souhegan. Amherst has roughly 5 times the number of residents as Mont Vernon does; it is possible to imagine a scenario where 3/5 of Mont Vernon voters approve a tax cap, but 3/5 of Souhegan voters do not. In that case, Mont Vernon residents might find that their taxes still rise more than the cost of inflation, because the cap only applies to one of the districts supported by their tax dollars.

Or, imagine the opposite. Maybe all Amherst residents want the cap, but Mont Vernon residents do not. Now, because of the size difference between the towns, SAU spending will be capped at 6% of appropriations across the three school districts, even though Mont Vernon voters didn’t want the cap. And it’s possible that a disproportionate share of the burden will fall on Mont Vernon, the one district with budget flexibility.

In other districts, tuition agreements might be a challenge. A number of small towns pay to send their high schoolers to Keene (Chesterfield, Harrisville, Keene, Marlborough, Marlow, Nelson, Spofford, Stoddard, Sullivan, Surry, West Chesterfield, Westmoreland, and Winchester). What happens if Chesterfield votes to implement a tax cap, but Keene does not? Keene could raise tuition rates at more than the cost of inflation (depending on the terms of the agreement and the timing of renewals, of course), which would mean Chesterfield has to spend a larger portion of its budget on tuition.

There are a number of potentially conflicting outcomes possible under this bill: SAUs with budget caps, funded by districts that don’t all have caps; taxes that rise despite a cap because not every district voted the same way; bigger districts forcing SAU caps on smaller ones because of sheer size, etc. These conflicting outcomes and complex questions would require staff time, likely at the SAU level, to figure out and track. Which could mean increased costs for administration to figure out increasingly complex requirements, but without the financial flexibility to actually pay for increased administration due to the caps.

SAU budgets

The definition of SAU budgets in the bill seems to conflict with the language in the question. The ballot question is clear: it is to cap spending at 6% of the appropriations of all districts in an SAU. In our SAU 39 case, we add up Mont Vernon, Amherst, and Souhegan’s budgets, calculate 6%, and that is the limit on SAU appropriations (how it is divided across districts is not dictated by the bill). But the list of items to be included in an SAU budget seems to go beyond what you’d find in a standard budget line item, and seems to include some district-level staff, who may not always be SAU staff. Calculating this budget as defined in the bill is not a simple task, and it’s going to require extra administrative support to ensure SAUs are complying with administrative spending caps.

Tax caps in the context of increasing uncertainty and complexity

Beyond the technical questions, there is a core challenge to tax caps: the legislature continues to pass legislation that makes budgets less predictable.

Take open enrollment. Under the version of HB 751 that emerged from the Committee of Conference, districts must allow up to 10% of students to enroll elsewhere and have their tuition paid by their resident district. What happens when a district gets an unexpected tuition bill that puts them over budget – and they can’t fill gaps because of a tax cap? How do districts build a budget within a tax cap when an unknown number of students might enroll elsewhere?

Then there’s HB 1817, which guarantees voucher students free access to public school courses and activities. What happens when a district has to pay a teacher to create another section of AP chemistry to meet demand from EFA students, but they have no authority to raise the money?

There’s also the special education funding bill, HB 1563, that reimburses districts for lower cost special ed cases but also phases out reimbursement for the highest cost cases, and requires detailed documentation to secure reimbursement. There will be inevitable unpredictability in special education budgets and increased need for administrative oversight, and districts won’t have the ability to fill the gaps. What if the increased administrative spending to comply with special education reporting requirements tips an SAU budget over 6%?

And of course, there’s HB 1610, which makes it harder for districts to raise and spend contingency funds. Without contingency funds, and under a tax cap, how are districts supposed to respond to increasingly unpredictable costs?

If lawmakers really wanted to lower property taxes, they would consider ways to meaningfully lessen the burden on school districts and to make budgets more predictable, rather than increasing the burden by applying an artificial cap that will require legal and administrative spending to manage and continuing to pile on new and expensive requirements.